Construction boom set to continue

26 Aug 2016, Featured, Industry Updates

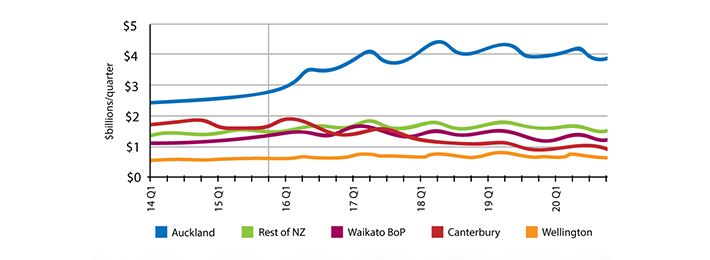

The 2016 National Construction Pipeline report forecasts the current construction boom will last for another five years, with Auckland the dominant player

The latest report predicts that the annual value of all construction is forecast to remain above 2015 levels for the next six years, reaching a peak of $37bn in 2017 – a 20% increase on the value of all construction at the end of last year.

Nationally, the value of residential construction increased 6% in 2015 and is forecast to increase a further 22% to a $21bn peak in 2017. After that, activity is expected to decrease slightly, but remain above 2015 levels throughout the forecast period.

The report also predicts an increase in higher density housing, with multi-unit dwellings representing 30% of consented dwellings in 2015. This figure is expected to increase to 40% by the end of the forecast period.

The value of all non-residential construction is forecast to increase by 20% during the 2016 – 2018 period to a peak of $16.8bn. The value is projected to remain at around $16bn per year for the duration of the forecast period.

Auckland accounts for half of expected growth

Residential construction in Auckland is expected to account for more than half of the national growth, increasing by $3.3b (or 53% of total national growth) to 2017.

It’s predicted that 94,200 new dwellings will be consented in Auckland between January 2014 and December 2021.

Auckland was the region with the highest ratio (44%) of multi-unit dwelling consented in 2015, with half of all consents forecast to be multi-unit by 2020.

Non-residential construction grew 4% over 2015 in Auckland and is projected to steadily increase by 49% to $7.3bn in 2018, due to a number of major projects planned for the region.

South of the Bombays

Waikato/Bay of Plenty

The two regions experienced a year of intense growth in 2015, with residential building increasing 24% by value. Activity is expected to peak in 2017 at $6.1bn and remain above 2015 levels until the end of 2020.

Non-residential construction in both regions is forecast to continue at a steady rate of around $2.5bn per year throughout the forecast period.

Wellington

Total construction activity in Wellington is expected to grow to peak in 2017 at around $2.8bn, remaining above 2015 levels for the remainder of the forecast. Residential building is expected to peak at around $1.2bn in the same year, while non-residential construction is expected to increase 10% to a peak of $1.6bn.

Wellington is the only reported region with non-residential construction by value at a higher level compared to residential building. This trend is expected to continue throughout the forecast period.

Canterbury

Building and construction activity levels in Canterbury have fluctuated a little after peaking in the final quarter of 2014. This is a result of residential consent levels dropping sharply in the first half of 2015, before rising again in the latter half of the year.

Non-residential construction is forecast to increase to $2.9bn per year in 2016/2017 and remain above $2.4bn until 2019, before steadily reducing to around $1.7b in 2021.

The Rest of New Zealand

Combined, the annual value of all building and construction in the other regions is forecast to rise to a gentle peak around 2019.

Non-residential construction activity is expected to slowly grow throughout the forecast period, with residential building forecast to rise by $0.5bn from 2015 levels to a gentle plateau of around $3.6bn from 2016-2019, before falling off slightly.

Otago has grown considerably; it is the largest single region in the ‘Rest of New Zealand’ region, and is gradually approaching Wellington’s level of activity.

Register to earn LBP Points Sign in