Managing business risk

11 Nov 2014, Featured, Insurance, Prove Your Know How

Most business owners don’t really understand how to put strategies in place to manage, avoid or transfer risk. This article, the first in a series, will help you assess the various risks your business faces and put processes in place to deal with them

Life used to be simple; it was about survival – finding enough to eat and avoiding being eaten by a sabre-toothed tiger!

But as a business owner in the modern world, there’s a lot to think about. One of the most fundamental problems is how to minimise the risks facing:

- Your business.

- Your customers.

- Your suppliers.

- The public.

- Yourself.

- Your family.

Four areas of risk

- Property

- Liability

- Financial

- Personal/family

Our experience over the last ten years has shown that thinking about risk in terms of these four areas works well for most building professionals. In the next four articles, we’ll cover each of these in more detail. Once you’ve identified all the various possible risks, evaluate them against these two criteria:

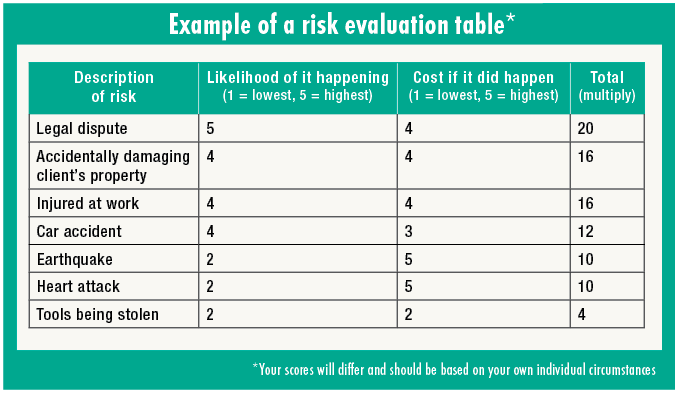

- The likelihood of it happening.

- The cost if it did.

In our experience, assessing risk in this way often takes away people’s worries, and they become much more positive about their situation. This process helps turn risks into a known quantity (not a heavy weight on your shoulders) that can be dealt with, whether this involves insurance, new processes, training or simply a decision to acknowledge the risk and do nothing.

What to do

The above table is one example of how to assess your own risk.

- Create a table for each of the four areas of risk, then list all the potential hazards that you can think of. It’s a good idea to do this with someone else, such as a business partner, spouse or even someone outside your business, such as your accountant. They add a different perspective and can often see things you can’t, because you’re so close to the business.

- Use your gut feeling and experience to decide how likely the particular hazard/event is and give it a score. Often thinking whether one risk is more or less likely than another helps choose a score.

- Next, consider the possible cost to you if the particular event was to happen. Would it be something you could handle, or would it break the bank? Again, considering the cost of each event compared to the others helps decide which are the most costly.

- Multiply the two scores to give a ranking of the risks you face.

- Rank all the risks on that final score. Write next to each one what you are doing to avoid, reduce or transfer that particular risk, starting with the ones with the highest score and working down.

By focusing on the risks with the highest score, you’re prioritising the areas that will have the most impact on you and your business.

“In our experience, assessing risk in this way often takes away people’s worries, and they become much more positive about their situation

Questions to consider for each risk

- Are you providing training in the right areas?

- Is your security adequate?

- Do you have the right procedures in place?

- What’s your plan B?

- Are the right risks insured?

Everyone has their own tolerance for risk; what you might think is low risk may be medium or high risk for another. However, by approaching your risk in this way, you’re able to prioritise and deal with it in a manner appropriate to your situation.

The next article will focus specifically on property, which includes the risk to buildings, vehicles, building sites and other material assets that can be lost or damaged.

About Builtin New Zealand

Builtin New Zealand is a specialist in insurance for the construction industry. For more information visit www.builtin.co.nz, email Ben Rickard at ben@builtin.co.nz or call him on 0800 BUILTIN

Register to earn LBP Points Sign in