How to manage risks – part I

18 Jul 2025, Employer Tips, Income, Insurance Tips, You

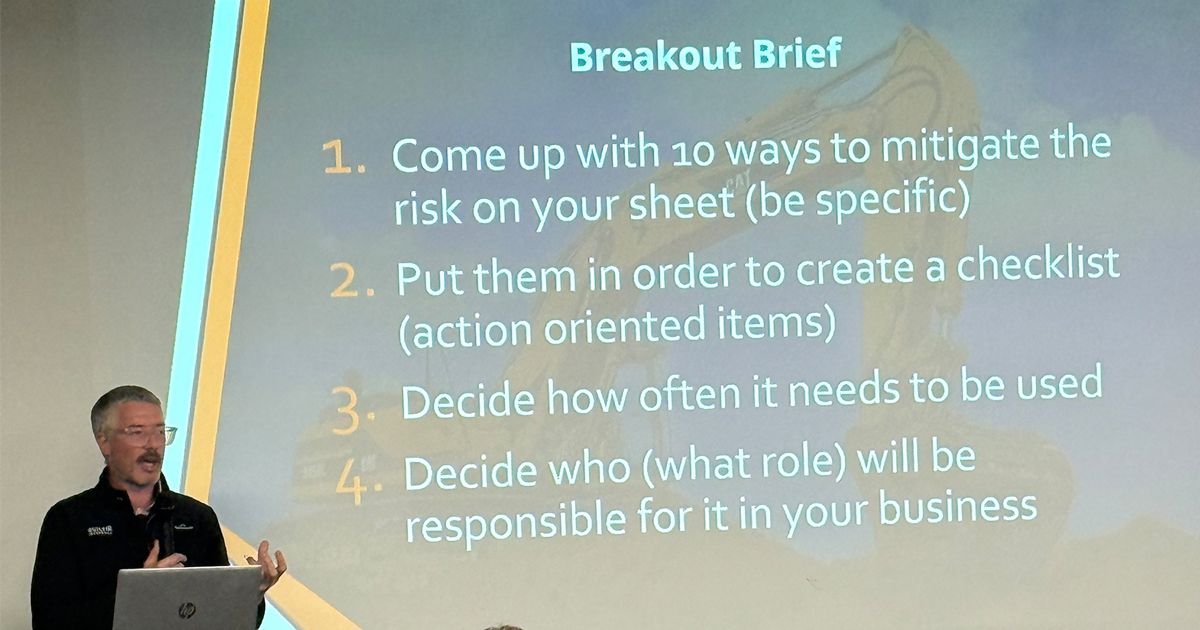

At the recent PlaceMakers LBP seminars in Wellington and Napier, construction risk and insurance expert Ben Rickard, from Builtin Insurance Brokers, had attendees break into groups and come up with ways to eliminate, reduce or manage the top five risk builders face (according to builders). This article is part one of two that reveals the results of those sessions

Risk 1 – Customers not paying or cancelling jobs

Customers not paying or cancelling jobs, cashflow issues and financial strain were named as the biggest risks that business owners face.

Construction businesses are more than twice as likely to fail compared to the average NZ business. Construction companies made up 26% of all liquidations in Q2 2024 (increasing +22% vs the prior year), despite making up only about 12% of registered companies.

Managing cashflow risk – checklist

- Get deposits from customers.

- Use a third party to manage payments (eg, escrow).

- Have appropriate insurance (unfortunately something that is not really feasible for small businesses).

- Credit check new customers, check references, research them on social media and at the Companies Office.

- Make sure your contracts are bulletproof.

- Take payments weekly or fortnightly, not monthly or on milestones – don’t leave a large payment at the end of the project.

- Have enough capital in the business to withstand short term issues.

- Communicate expectations to customers clearly and early, then regularly through the job.

- Always use Construction Contracts Act-compliant payment claims and schedules.

- Get variations in writing every time.

When should it be used

The overwhelming response from builders at the LBP Seminars was that the actions on the checklist should be done before quoting, at the beginning of every job and regularly (eg, monthly) after that.

Who is responsible

Attendees maintained it should be the business owner’s responsibility to follow this checklist.

Risk 2 – Illness or injury affecting the business owner

Did you know non-fatal injuries are 50% more common in small businesses? And that self-employed people are around 15% more likely to get injured than employees are?

If a business owner gets sick or injured, this can significantly hamper the ability of the business to continue trading successfully. Below is a checklist to help you avoid this.

Stay well for your business – checklist

- Prevention (good wellness practices, regular check-ups, living a healthy lifestyle – including drinking habits, diet and exercise).

- Have a succession plan and/or trained back-up resource that can step in if needed.

- Make sure paperwork is always up to date (not just in your head).

- Allow for delays due to illness within contractual terms.

- Have income protection and/or key person insurance.

- Set aside ‘rainy day income’ – have good cashflow, so you can ride it out.

- Ensure key staff and sub-trades have access to necessary systems (eg, store documents in the cloud).

- Take health and safety (prevention of accidents) seriously.

- Have an up-to-date list of contact details for everyone.

- Make sensible decisions around sport and recreation activities.

- Have regular team meetings, so everyone is up to speed, and communicate regularly with staff and customers.

- Have a good work/life balance and take time out when it’s needed for your mental health.

- Delegate as much as you can to reduce stress and avoid becoming a knowledge bottleneck.

When should it be used

Attendees said at the start of every project, daily, monthly or yearly depending on the task.

Who is responsible

Builders reported that either the business owner or a partner, manager or second-in-command need to make sure the above happens.

Builtin are New Zealand’s Construction Risk Management Experts. For more information visit www.builtin.co.nz, email Ben Rickard at ben@builtin.co.nz or call him on 0800 BUILTIN.

Register to earn LBP Points Sign in